The Largest End-to-End Omnichannel Enabler In Southeast Asia

Trusted by the world’s leading brands

SE Asia’s Leading

End-to-End Omnichannel Enabler

We are the leading enabler in Southeast Asia, trusted by the world’s top brands. Our end-to-end enablement solution allows you incredible speed-to-market time, regional expertise, and global standards. Built to scale, without all the additional costs and pain of having to build in-house infrastructure.

COMPETE FASTER by

#1 E-commerce Business Services in SE Asia

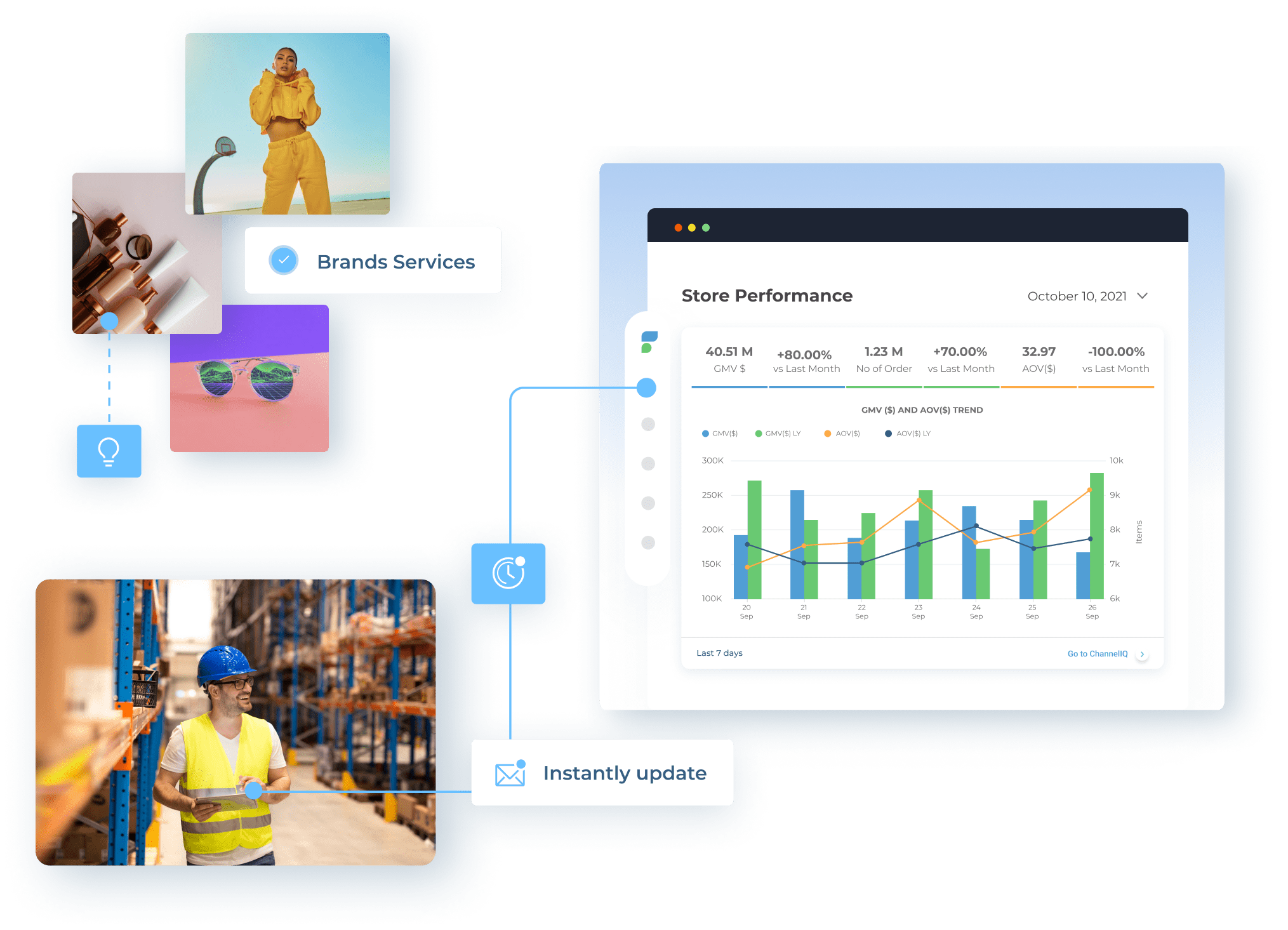

Managed Services

Our e-commerce Managed Services makes it easy for your brands to enter a market and scale your online business without the costly need of building your infrastructure or training internal teams. Our Managed Services are cost-efficient and built to scale with the most innovative team in the region. Partner with aCommerce to get the best results for your e-commerce business.

Online Store Operations

Enhance your e-commerce ecosystem, boost conversions and create a seamless experience with our data-driven strategies.

Learn more

Online Brand Management

Maximize your brand's performance online and ensure optimal product presentation and lead marketing campaigns.

Learn more

E-commerce Marketing

Our intuitive performance marketing solutions will enable you to gain deeper insight into your customers and adapt your strategy to boost.

Learn more

Fulfillment Centers

We empower you to manage the complex and dynamic supply chain. Gain full control of the entire logistics process across multichannel selling platforms.

Learn more

Customer Service Solutions

Our experienced team of customer care experts is ready to assist your shoppers in their local language so you can drive ROI in the language that your market speaks.

Learn more

Online Store Development

Optimize every touchpoint and capture audiences by creating localized and engaging and converting experience across all your ecommerce channels.

Learn more

Consultation and Training

From online local branding to creating an omnichannel approach, our team of experts will help you gain control over your brand.

Learn moreThe harness the empower of e-commerce

Simplfied and Unified

E-commerce Enablement Platform

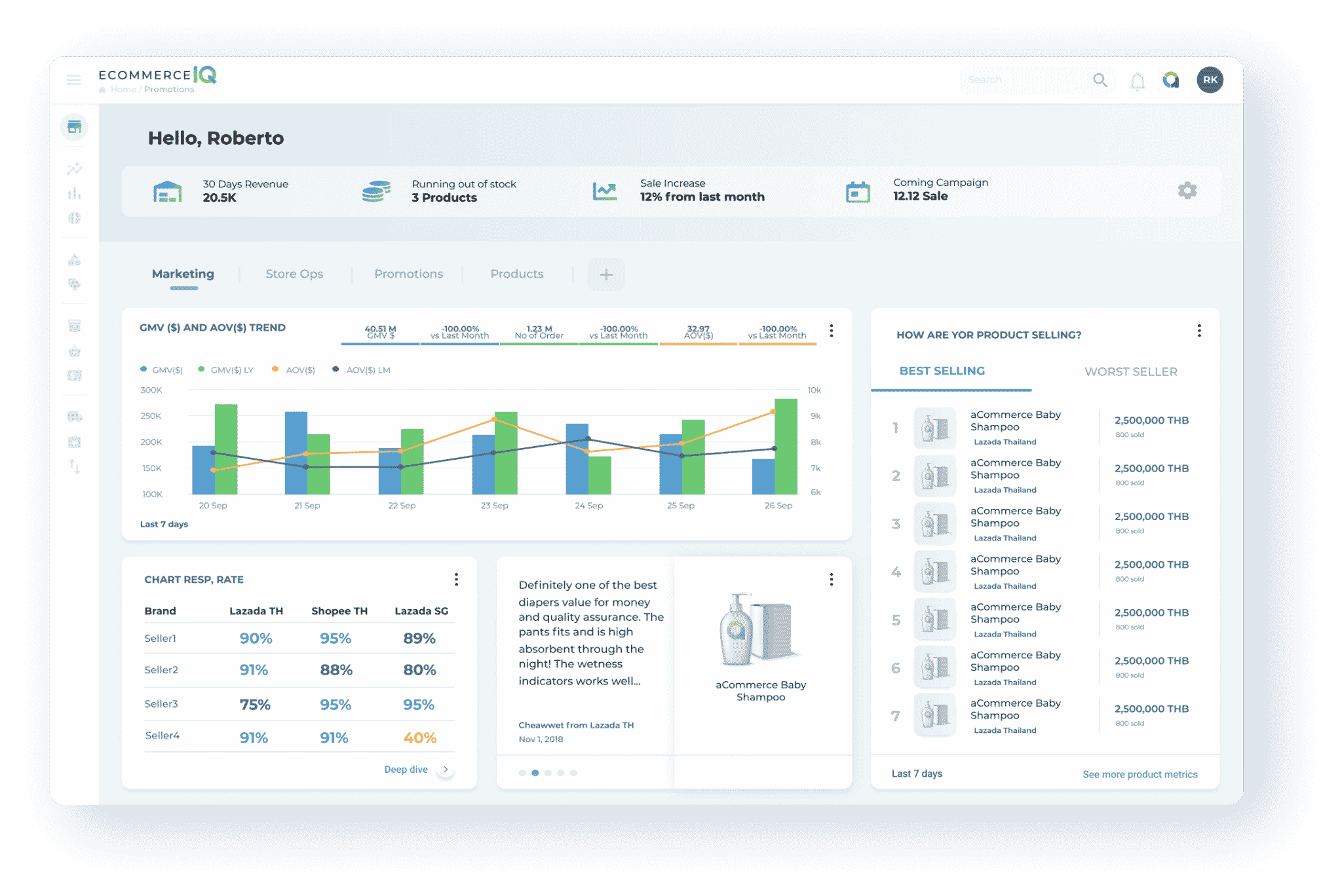

EcommerceIQ is a cutting-edge e-commerce management solution by aCommerce that provides you with a 360° view of their business and a complete toolset to service all business units and e-commerce processes including accounting, merchandising, performance marketing, account management, fulfillment and logistics, omnichannel order management, and business intelligence.

360° view of your business

All-in-One E-commerce Management Platform

Using EcommerceIQ, brands can easily monitor and control every aspect of their e-commerce business across multiple channels – all in our unified platform.

Make smarter decisions about your business in real-time and hit sales targets with ease.

Sell your products anywhere online and grow your revenue across multiple channels by switching to our enterprise-level e-commerce management platform.

Market Insights

Compete smarter with the leading marketpalce analytics in Southeast Asia.

Multi Stores Management

Kick start and execute your online direct to consumer (D2C) business with lowest entry barrier.

Logistics Management

Increase your last-mile 3PL partners delivery efficiency with a smart logistics tool.

Engagement Management

Join a unified customer data & the right customer persona for a personalized online customer experience.

Client & Business Analytics

Gain actionable insights through a 360° ecommerce performance & operational insights dashboard.

Omni-Channel & Order Management

Grow sales efficiently through data-driven multichannel order management.

Recent News

Stay up to date

with our news.

Southeast Asia Market Potential

There has never been a better time to scale your e-commerce business

Million

New Online Users

In Southeast Asia In 2020

Million

Online

Consumers

Partners

Meet our clients

Want to explore more?

E-commerce can be complicated, simplify it with aCommerce end-to-end enablement.